What is a ULIP, Meaning and its Benefits?

-

Our Products

- Capital Secure+ - A Combination Of Market-Linked And Guaranteed Returns

- Edelweiss Tokio Life –Wealth Rise+ – A double-advantage ULIP

- Edelweiss Tokio Life – Premier Guaranteed Income – A guaranteed income plan

- Edelweiss Tokio Life –Wealth Secure + - A new generation ULIP

- Edelweiss Tokio Life- Zindagi Protect - A Comprehensive Term Plan

- All Products

What is a ULIP, Meaning and its Benefits?

12/16/22 11:34 AM

Blog Title

2382 |

Life insurance and investments are two of the most crucial aspects of your financial portfolio, but sometimes, maintaining the balancing act between the two can be tricky and time-consuming. This is where ULIPs can simplify things for you.

ULIP stands for Unit-Linked Insurance Plan, a life insurance product that doubles as an investment plan. In a ULIP, you get life cover for a sum assured, just like a traditional term plan. Additionally, you get the opportunity to invest in market-linked financial instruments to create wealth over the long term. This dual nature makes ULIPs a popular option among investors of all types, and they can be valuable additions to your portfolio. This article will explain ULIPs, how they work, and their chief benefits.

How does a ULIP plan work?

In a ULIP plan, a portion of your premium is invested in market-linked instruments, while the remainder is utilized to provide you with life insurance. So, at maturity, you get returns on the money invested in the market. And in the event, God forbid, of your untimely death during the policy period, the sum assured, along with the current value of funds, will be given to your nominee.

This way, you will be able to invest money in the market for better returns and also have assurance in case things go out of the plan.

The insurer pools the money from multiple investors and then puts it proportionately into the various funds. These funds are financial instruments that invest in specific market-linked assets, like stocks, government securities, etc. This is similar to how mutual funds work; they too have one or more asset classes that they invest in. These asset classes define the risk and the returns that can be expected from the fund.

For example, if you are an investor seeking lower risk, you may opt for debt funds, while equity is preferred by investors willing to take higher risks. If you are someone looking for a combination of equity and debt funds where risk is moderate and returns are higher than debt funds, then balanced funds are the right choice for you! Let’s understand this in detail below.

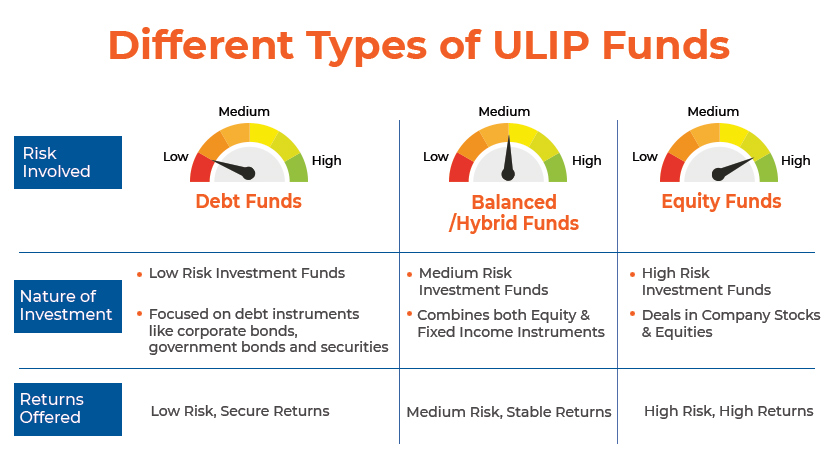

ULIPs provide a diverse selection of fund options, ranging from high-risk to low-risk. Furthermore, they provide the possibility of switching funds to deal with market volatility and optimize profit. For example, Edelweiss Tokio Life Insurance offers 7 diverse fund options to choose from, which can be categorized into the following three types:

● Equity Funds: Equity funds in ULIPs, as the name implies, invest predominantly in the stock market. This entails investing in publicly traded equity stocks. The fundamental goal of equity funds is capital appreciation because the market-linked returns associated with equity stocks might be higher in the long run. However, you should remember that , equity funds are often riskier than other ULIP funds, but they also have the potential for higher returns.

● Debt Funds: These funds invest in the debt market, which comprises various debt-based products such as government securities, corporate bonds, and other fixed-income instruments. This is why debt funds have low risks.

● Balanced or Hybrid Funds: Hybrid or Balanced Funds invest in equity and debt to provide healthy returns without taking on many risks.

Your choice of funds will depend on your risk tolerance and financial objectives. For example, equity funds have a higher element of risk, but they also carry the potential for higher returns. On the other hand, debt funds are more secure but offer lower returns comparatively. Finally, hybrid funds have a moderate amount of risk with similar returns.

The investments in a ULIP can be self-managed or managed by fund managers from the insurance company, eliminating the need to track them constantly. The choice between these two fund management options depends on how much involvement you desire.

ULIPs are generally viewed as a long-term financial product for accumulating wealth as it comes with a 5-year lock-in period, during which you cannot access your funds. However, after this lock-in period ends, you can make partial withdrawals from your accumulated funds.

Now that we understand the essential workings of a ULIP, let us look at the benefits of choosing a ULIP plan.

What are the benefits of investing in ULIPS?

A ULIP plan provides numerous benefits as a hybrid insurance product:

- Dual Advantage of Investment and Insurance: ULIPs mix investment and insurance benefits. The plan's insurance component provides you with life insurance protection. Maturity benefits are paid if you outlive the plan's term. If, on the other hand, you do not survive the policy, your beneficiaries will get death benefits to help them deal with any financial difficulties resulting from your unfortunate demise. Furthermore, ULIPs allow your investment to increase over time, culminating in a sizable corpus that you may rely on later in life.

- Option to Choose the Desired Life Cover: You can select the amount of life cover that you want. However, the amount of life cover can vary from policy to policy.

- Freedom to Choose the Investment Type: You can invest in any of the three fund types provided by ULIPs based on your risk tolerance and investment objectives. For example, if you have a high risk tolerance and desire greater returns on investment, you can participate in the equity fund. Alternatively, you might invest in debt funds if you want a consistent return on investment. Furthermore, you can switch from one fund type to another, to maneuver your funds as per market conditions and fund performance.

- Opportunity for Goal-Based Planning: ULIPs are particularly tailored to meet your long-term financial goals. They can assist you in securing financial goals such as preparing for your child's education, retirement planning, wealth creation, and so on.

- Additional Tax Benefits : Because unit-linked insurance plans also provide life insurance, you can benefit from tax breaks under these plans. The policy's premiums, up to ₹1.5 lacs a year, are tax-free under Section 80(80C) of the Income Tax Act of 1961. Furthermore, under Section 10(10D), the maturity and death benefits are exempt from taxation.

Conclusion

Are ULIPs the right choice for you?

Because there are so many investment options available on the market, deciding on the best one is usually a challenge. Whether ULIPs are a better investment alternative than others is a recurring question. However, before deciding on any financial product, it is critical to find the answers to the following queries-

➔ What do you hope to accomplish with your money?

➔ What is your risk tolerance?

➔ What is your financial goal? Whether you want to start retirement savings or have a backup plan for any form of emergency that may arise.

➔ How long will the investment last?

➔ Do you require life insurance?

If you are certain about all these things and know what you want to achieve, then you can decide if a ULIP is the best investment plan for you or not Additionally, individuals who desire to build wealth over time while also receiving insurance coverage may consider investing in a ULIP. To sum up, these plans work as a good investment choice for those who are new to the market and want to benefit from capital appreciation through investing in market-linked assets.

Siddhant Dubey - Writer & Photographer

Siddhant works as a freelance content writer who is interested in a wide range of spheres from photography and personal finance to cooking. He is also an aspiring photographer striving to showcase life around him through his vision.

Related Blogs