Wealth Gain +

-

Our Products

- Capital Secure+ - A Combination Of Market-Linked And Guaranteed Returns

- Edelweiss Tokio Life –Wealth Rise+ – A double-advantage ULIP

- Edelweiss Tokio Life – Premier Guaranteed Income – A guaranteed income plan

- Edelweiss Tokio Life –Wealth Secure + - A new generation ULIP

- Edelweiss Tokio Life- Zindagi Protect - A Comprehensive Term Plan

- All Products

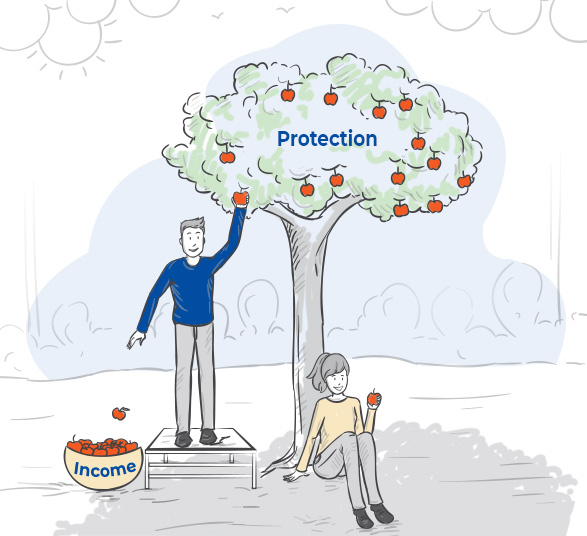

Unlock A Gains-filled Zindagi for Your Future

you back from experiencing them! That is why we’ve created Edelweiss

Tokio Life Wealth Gain+ - a ULIP plan designed to give you dual benefits

of Life Cover and Wealth Accumulation with no unnecessary charges.

Take a step ahead to secure your goals

View Download

View Download

Reasons Why This Plan Will Help You Plan For The Future

Nil Allocation Charges

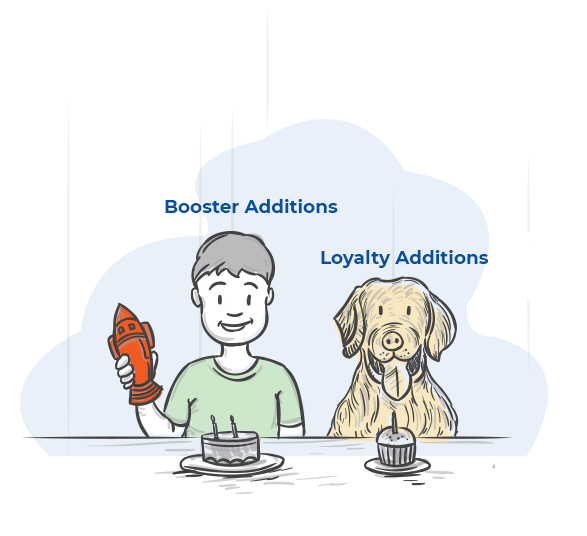

Li’l Extra from Our End

Li’l extra from your end

Choice of 7 Funds

Making Plans For The Future In 3, 2, 1 - Go!

More Products You'd Love to Explore

Capital Guarantee¹: Assurance Amidst Market Fluctuations

Market-linked returns, with an additional benefit of guaranteed¹ return of your total invested premium at maturity

Benefits of market-linked returns and guaranteed¹ lumpsum in one plan

Enhanced cover option with sum assured & booster additions

Little Star Benefit option to protect your child’s future

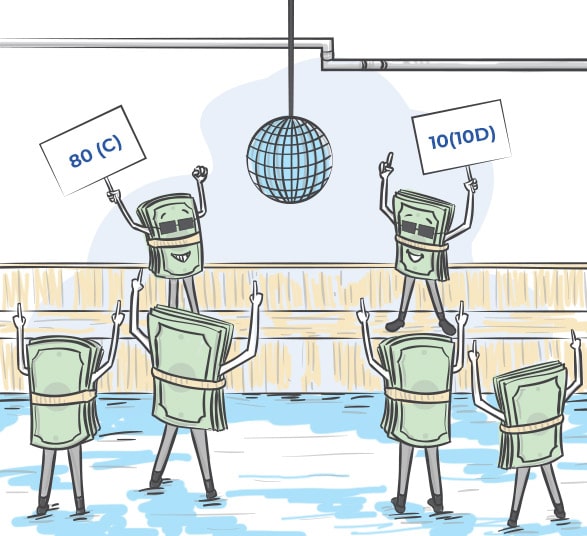

Tax benefits³ u/s 80c & 10(10d) to shield your savings

Har Sapna Karo Poora with Guaranteed¹ Savings!

Guaranteed¹ returns, enhanced cover option, tax benefits³, and more… all with premiums just Rs. 3,000/month^².

Choice to receive guaranteed¹ returns as lumpsum or in 5 equal annual instalments

Enhanced Cover option to secure your family with 20x the premium^⁴ paid

Guaranteed¹ savings & life cover for a policy term as high as 40 years

Family Income Benefit option to ensure your family doesn’t have to compromise on dreams

Future Guaranteed¹ Income, now possible!

Makes sure nothing gets in the way of you and your dreams.

Guaranteed¹ Income + Protection + Tax Benefits³ in one plan

Pick from 4 plan options basis life goals – Lumpsum, Short Term Income, Long Term Income & Retirement Income

Family Income Benefit option ensures your family doesn’t have to compromise dreams

6 Riders available to enhance your plan⁹

Need expert advice?

We are always there for you !

For queries, write to onlinesales@edelweisstokio.in

Contact us on 022 6611 6054

Related Articles & Resources

0- Provided the premium paying term is more than or equal to 10 years.

1- Applicable only if all due premiums are paid and the policy is in-force.

3- As per provisions of Income Tax Act, 1961. Tax benefits are subject to changes in tax laws.

The Linked Insurance Products do not offer any liquidity during the first five years of the contract. The policyholder will not be able to surrender/withdraw the monies invested in Linked Insurance Products completely or partially till the end of the fifth year.

Disclaimer: Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Edelweiss Tokio Life Insurance is only the name of the Insurance Company and Edelweiss Tokio Life – Wealth Gain+ is only the name of A Unit Linked, Non-Participating, Individual, Life Insurance Product and does not in any way indicate the quality of the contract, its future prospects, or returns. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Please know the associated risks and the applicable charges from your Personal Financial Advisor or the Intermediary or policy document of the Insurer. The premium paid in unit linked life insurance policies are subject to investment risk associated with capital markets and the unit price of the units may go up or down based on the performance of investment fund and factors influencing the capital market and the policyholder is responsible for his/her decisions. Tax benefits are subject to changes in the tax laws. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

IRDAI Reg. No.: 147. CIN: U66010MH2009PLC197336. UIN: 147L061V03

ARN: WP/3429/Oct/2023