Forever Pension

-

Our Products

- Capital Secure+ - A Combination Of Market-Linked And Guaranteed Returns

- Edelweiss Tokio Life –Wealth Rise+ – A double-advantage ULIP

- Edelweiss Tokio Life – Premier Guaranteed Income – A guaranteed income plan

- Edelweiss Tokio Life –Wealth Secure + - A new generation ULIP

- Edelweiss Tokio Life- Zindagi Protect - A Comprehensive Term Plan

- All Products

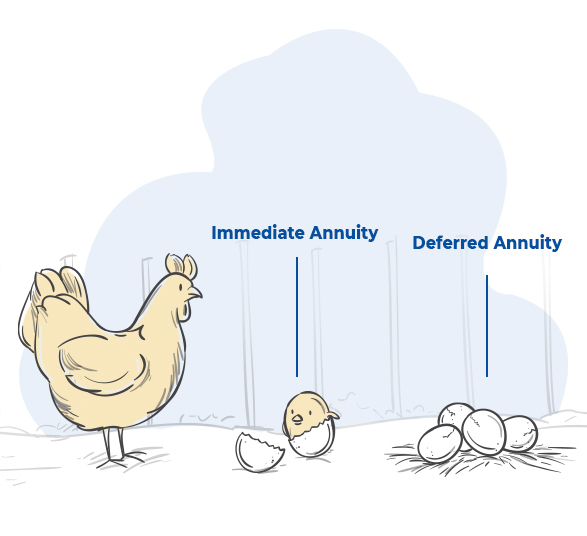

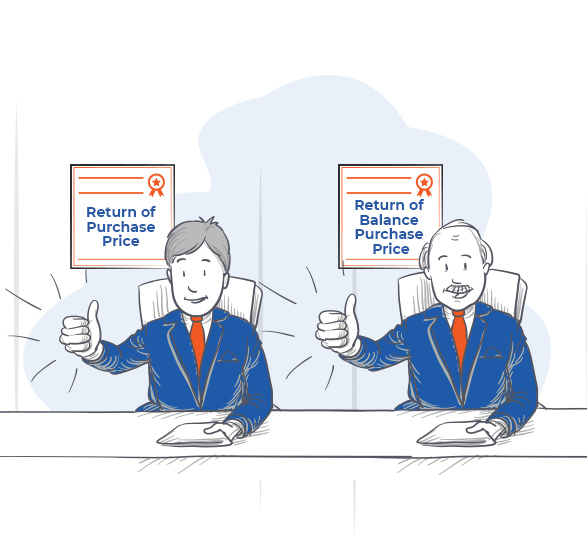

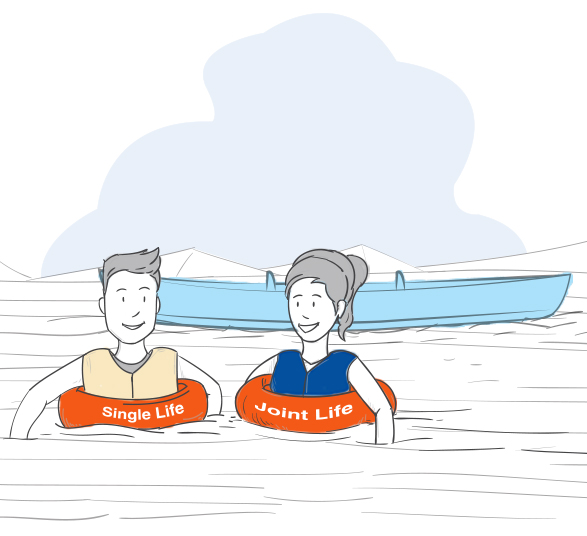

Edelweiss Tokio Life - Forever Pension

which provides you with guaranteed¹ income in your golden years to

indulge in life's necessities without any compromises. A plan which

takes away your concern of generating regular income and how you

would spend your retirement years.

Take a step ahead to secure your retired life

View Download

View Download

Why should you buy this plan?

He was very much clear about the issue and the importance of it.. Thanks rohit

Anisha Shashidharan

(sr.associate)

Your customer support is doing excellent job.keep up the good work.

Nilesh Pawar

(manager)

We are always there for you !

For queries, write to onlinesupport@edelweisstokio.in

1- The word “Guaranteed” and “Guarantee” mean that annuity payout is fixed at the inception of the policy

Edelweiss Tokio Life – Forever Pension is only the name of a Non-Linked, Non-Participating Single Premium Individual General Annuity Plan and does not in any way indicate the quality of the plan, its future prospects or returns. Please know the associated risks and the applicable charges from your Personal Financial Advisor or the Intermediary. Tax benefits are subject to changes in the tax laws. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

IRDAI Reg. No.: 147. CIN: U66010MH2009PLC197336. UIN: 147N068V02

ARN No : WP/3448/Oct/2023