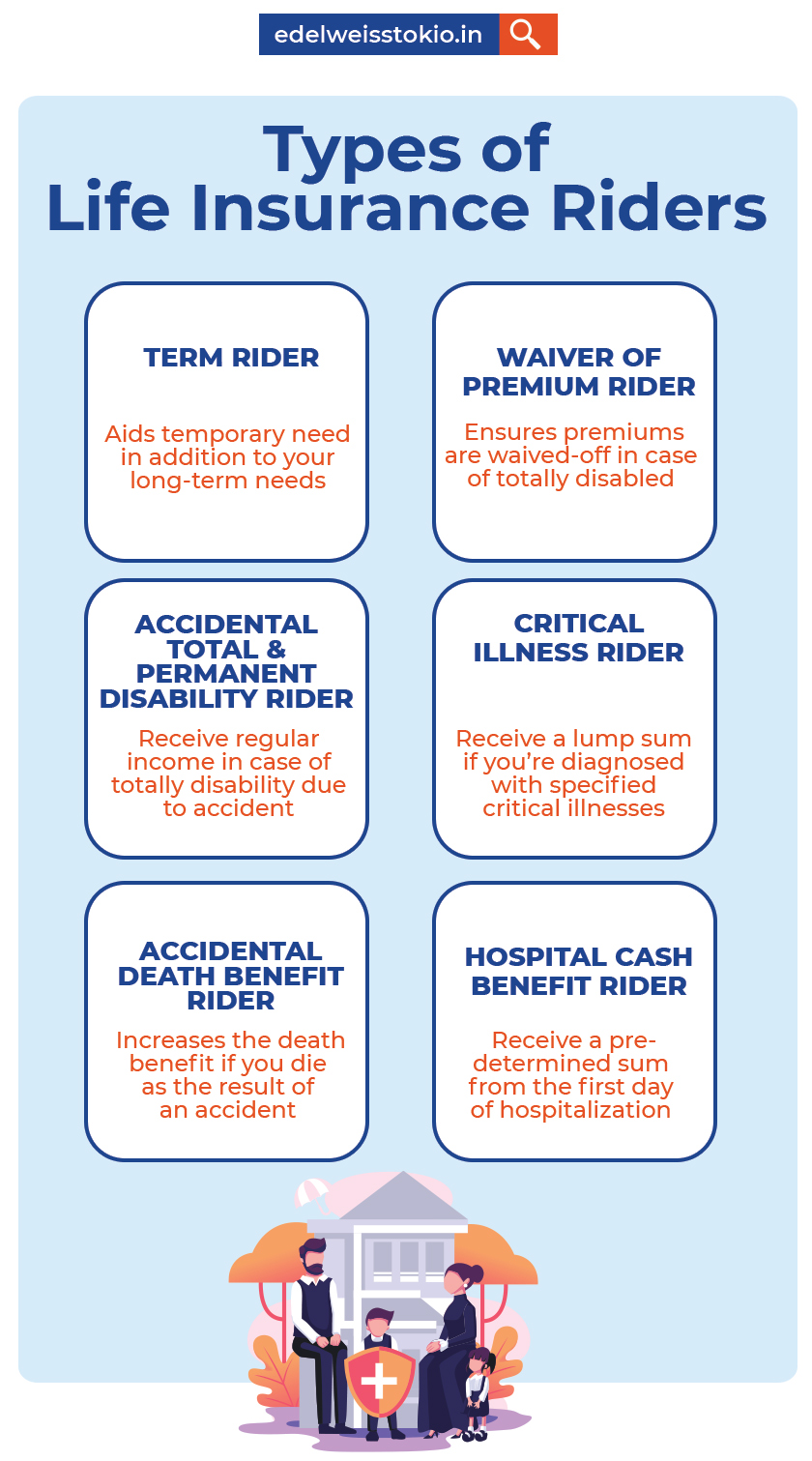

Riders

-

Our Products

- Capital Secure+ - A Combination Of Market-Linked And Guaranteed Returns

- Edelweiss Tokio Life –Wealth Rise+ – A double-advantage ULIP

- Edelweiss Tokio Life – Premier Guaranteed Income – A guaranteed income plan

- Edelweiss Tokio Life –Wealth Secure + - A new generation ULIP

- Edelweiss Tokio Life- Zindagi Protect - A Comprehensive Term Plan

- All Products

Riders

12/13/22 2:35 PM

Blog Title

2862 |

Grace Period is the additional time you get as a policyholder after the due date to pay your premium. This period is put in place so that you can avoid losing life coverage and other features of your policy, as well as avoid incurring any penalties in case you are a bit late on policy renewals. According to IRDAI norms, the grace period for life insurance varies depending on the premium payment terms, which might be yearly, half-yearly, quarterly, or monthly.

As many people lead busy lives, missing the due date for premium payments is not uncommon. It can be due to numerous other factors as well, like financial/ personal problems, and insurance companies are aware of it. That is why you might get multiple reminder messages from your insurer as the due date approaches. Still, if you are not able to make the deadline, the grace period kicks in and offers some additional time.

In India, there are various premium payment options available for life insurance:

- Single-Premium Payment: A single premium payment is made in the form of a lump sum, one-time upfront payment when the plan is purchased. This premium payment is regardless of the duration of the policy you choose. This offers a never lapse policy advantage as there will never be a scenario of non-payment of policy premiums. Hence, grace period is not applicable here.

- Regular Premium Payment: Depending on your needs, you can pay the premium amount yearly, half-yearly, quarterly, or monthly. Since the premiums are spread over a period of time it offers flexibility and avoids any burden, or one-time financial strain. Some policies also give you the ability to choose the term of your premium payments, i.e., for how long you would be paying the premium. It can be equal to the policy term but also shorter. If it is shorter, then it’s called limited premium payment. However, the premiums might be on a higher side, but it turns out to be advantageous for someone who do not wish to keep paying premiums for a longer period of time.

Furthermore, if you choose annual, half-yearly, or quarterly premium payment modes, the maximum grace period for renewal of the policy is 30 days. However, in the case of monthly premium payments, you are eligible for a grace period of 15 days. This might also depend on the insurer you are choosing for your life insurance policy.

If you skip or fail to pay the term insurance premium amount and do not renew your plan during the grace period for any reason, the insurer will cancel the plan. This means that you and your loved ones will no longer be financially protected. A lapsed policy is a significant loss for you because the money you paid will not be reimbursed, and you will also lose all insurance coverage.

However, if you die unexpectedly while in the middle of the grace period, your loved ones are eligible to receive the death benefit/payout as per the policy's terms and conditions. Please note that the insurer will deduct any unpaid premiums while paying out the death benefit to your nominees.

Aastha Mestry - Portfolio Manager

An Author and a Full-Time Portfolio Manager, Aastha has 6 years of experience working in the Insurance Industry with businesses globally. With a profound interest in traveling, Aastha also loves to blog in her free time.

Related Blogs

Exploring A Safe and Secure Way to Generate Second Income? We have the Answer!

I Have Cleared My Financial Liabilities. Should I Surrender My Life Insurance Policy?