Premium Payment Terms | Types | Benefits

-

Our Products

- Capital Secure+ - A Combination Of Market-Linked And Guaranteed Returns

- Edelweiss Tokio Life –Wealth Rise+ – A double-advantage ULIP

- Edelweiss Tokio Life – Premier Guaranteed Income – A guaranteed income plan

- Edelweiss Tokio Life –Wealth Secure + - A new generation ULIP

- Edelweiss Tokio Life- Zindagi Protect - A Comprehensive Term Plan

- All Products

Premium Payment Terms | Types | Benefits

11/9/23 10:53 AM

Blog Title

11175 |

The Premium Paying Term or PPT is the period for which you must pay the required premiums for your life insurance policy. In other words, it is the term for payment of premiums. Generally, in case of Term Insurance, the premium payment term is usually equal to the policy term. However, some insurance policies like Guaranteed Income Plans or ULIPs, allow the policyholder to select a premium-paying term shorter than the policy term. These policies may also offer you flexibility in terms of choosing the premium payment term, for example 5, 8, 10 & 12 years.

Some insurers allow the insured to get insurance benefits even if they cease paying premiums after a particular duration of time by turning the standard insurance policy into a paid-up policy.

Premium Paying Term vs Policy Term

Premium paying term and Policy Term are two different things and are often confused as one.

| Premium Paying Term | Policy Term |

|---|---|

The time period within which you pay your premiums. |

The total time period of your life insurance policy. |

Your policy will lapse if you fail to pay premiums during this term. |

If you have finished paying off your premiums, then your policy cannot lapse. Life cover will continue until the very end of your policy term. However, you may choose to surrender the policy at any time during the policy term. |

Is always shorter than the policy term, unless you opt for regular pay, in which case it will be equal to the policy term. |

Can never be shorter than the premium paying term, signifies the total duration of your life insurance policy. |

Why is Premium Payment Term Important?

Deciding the right premium payment term for your policy is extremely important for budgeting your finances. Do you have enough income to pay off the entire premium in just a few years? Or would large payments be too hectic for your budget? Do you want to pay off your premiums as quickly as possible or do you not mind regularly paying a small amount every single month? Answering all these questions will help you select a plan with the right premium payment term for you.

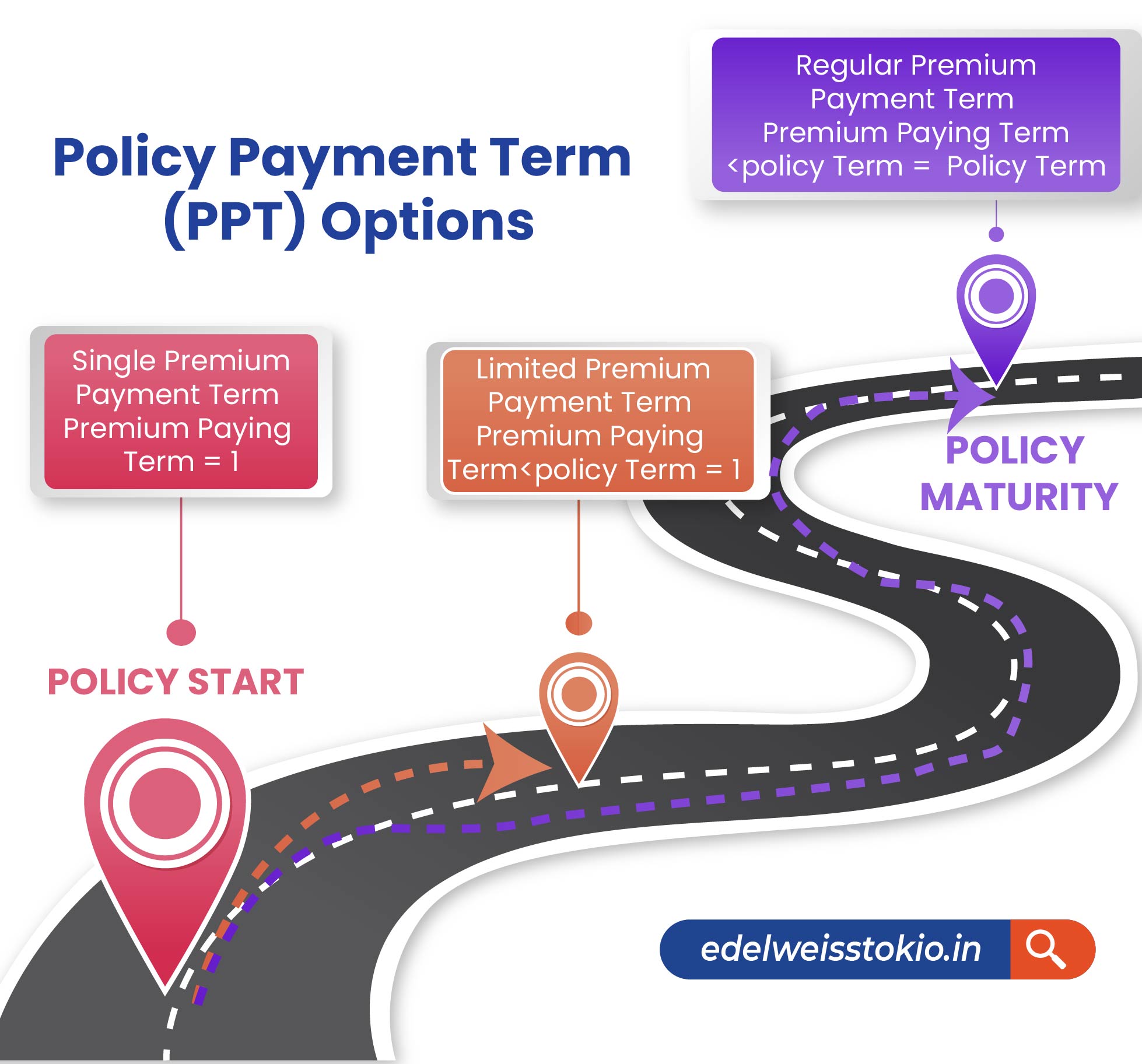

Types of Premium Payment Terms

There are pros and cons to each type of premium payment term, and you need to determine what term is best suitable for your budget. The various types of premium payment terms are listed below:

- Regular Premium Payment Term: If the premium payment term is the same as or equal to the policy term, you must pay premiums for the whole policy term. This is referred to as regular premium payment. For example, if the policy period is 20 years, you must pay premiums for 20 years.

- Limited Premium Payment Term: The other possibility is that the premium paying term is shorter than the policy term. In such cases, you pay premiums for a limited time, but the life insurance coverage continues until the policy term expires. For example, you may select a policy duration of 20 years but pay premiums only for the first ten years.

- Single Premium Payment Term: The entire premium amount is paid as a lump sum in one instalment for the policy coverage till the end of the policy. For example, you may select a policy duration of 60 years but pay premium once as a single premium.

- Flexible Premium Payment Term: Flexible premium payment term basically means that you can adjust your premium payment amount and frequency (to a certain limit specified by the insurer) according to your needs. This flexibility allows you to pay premiums safely even during financially difficult times. Flexible premium payment option is an enhancement of the limited pay model.

In regular and limited payment term options, premium payments can be made monthly, quarterly, bi-annually, or annually.

How to Choose the Right Payment Term?

The right payment term for you will depend on how quickly you want to pay off your premium, and how much money you are willing to spend on insurance in the short term.

Benefit of Single Pay

If you don’t want the burden of paying premiums periodically, then just opt for the single pay model. With single pay, you just have to pay a lumpsum amount at the beginning of the policy to enjoy the benefits for the rest of the term. However, keep in mind that single pay premium policies generally do not offer the same benefits and coverage as limited or regular pay policies.

Benefit of Regular Pay

Regular pay is best if you do not mind paying premiums until the very end of your policy term. The periodic premium payments for Regular pay are generally more affordable than limited pay, making it the better model of payment if you are on a tight budget.

Benefits of Limited Pay

If you do not want to pay premiums for the entirety of your term but still want all the benefits of a regular pay policy, then the limited pay model is ideal for you. With limited pay, you can pay off your premiums as quickly as possible. Once your premium has been paid off, you can enjoy the policy’s life cover and other benefits without having to pay a single additional dime.

Moreover, the total premium amount payable in limited pay is generally smaller when compared to regular pay, though this might not always be the case. The main downside of limited pay model is that your periodic premium payments will be much more expensive, as you are paying off the entire premium amount in a much short timeframe.

Siddhant Dubey - Writer & Photographer

Siddhant works as a freelance content writer who is interested in a wide range of spheres from photography and personal finance to cooking. He is also an aspiring photographer striving to showcase life around him through his vision.

Related Blogs